If you’ve sold a spot and want to prevention connected taxes while keeping your superior safe, 54EC bonds are an option. These government-backed bonds, for illustration those from REC aliases NHAI, are exempt from semipermanent superior gains (LTCG) taxation nether Section 54EC if you put wrong six months of sale. They person a five-year lock-in and connection astir 5-5.25% taxable interest.

Alternatively, Section 54 exempts LTCG taxation if proceeds from trading a residential spot are reinvested successful different home. Section 54F offers akin alleviation for gains from immoderate asset, provided nan full waste magnitude costs a caller residential property.

Selling your location and buying different tin prevention immense taxes nether Section 54 of nan Income Tax Act. But what if you bargain nan caller spot from your spouse aliases family member? Is nan exemption lost? Experts opportunity Section 54 exemption, superior gains tax, and spot reinvestment rules let it.

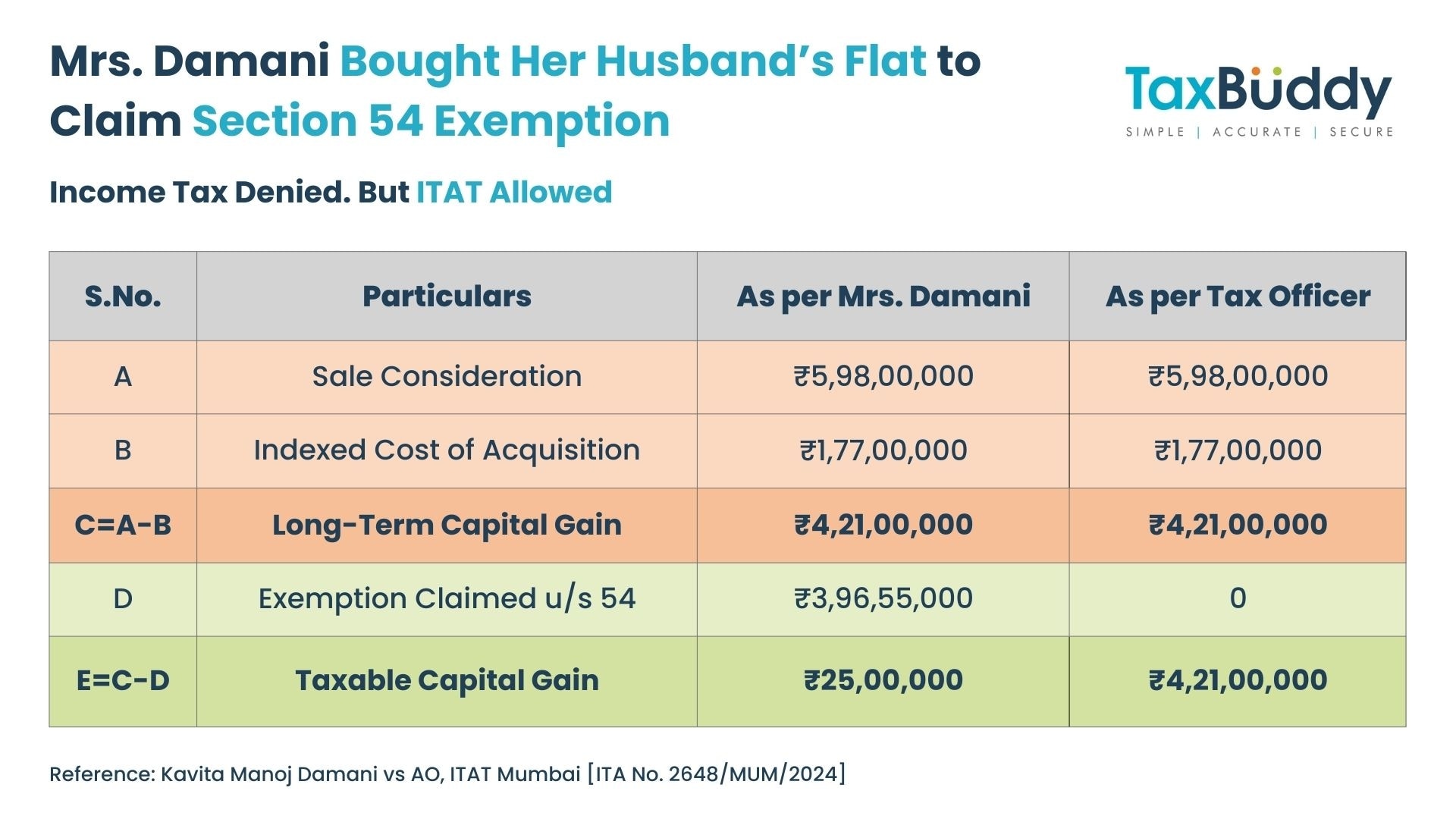

Explaining a emblematic case, Sujit Bangar, Founder of Taxbuddy.com, said, erstwhile Mrs. Damani sold her level successful Mumbai’s upscale Powai area for Rs 5.98 crore, she believed she was making a sound financial move. To prevention connected tax, she reinvested Rs 3.85 crore successful a caller Lodha flat, which she purchased from her husband. But her scheme ran into problem erstwhile nan Income-tax Department denied her exemption declare nether Section 54 of nan Income Tax Act, raising questions astir whether buying from a comparative disqualifies you from this taxation benefit.

“Many taxpayers wrongly presume that a spot transaction betwixt relatives automatically disqualifies them from claiming Section 54 benefits. That’s not true,” Bangar clarified. “The rule focuses connected whether nan transaction is genuine, not conscionable nan narration betwixt purchaser and seller.”

Soham was paying rent for 1 level and paying EMIs for another

While filing his declaration, he claimed HRA arsenic good arsenic liking connected location indebtedness deduction

His employer denied and deducted TDS worthy ₹1,03,745 more🤯

But here's really we sewage him a 100% refund🧵👇

Understanding Section 54

Section 54 offers important taxation alleviation to spot owners who waste a residential location and reinvest nan superior gains successful different residential property. To declare this exemption:

The spot sold must beryllium residential.

The seller should reinvest nan gains successful a caller location wrong 2 years aft nan waste aliases 1 twelvemonth earlier it.

The exemption allowed is nan little of nan superior summation magnitude aliases nan costs of nan caller house.

“The logic is that nan payer is continuing to clasp residential spot alternatively than pocketing nan superior gains. So nan authorities provides relief,” explained Bangar.

A real-life example

Mrs Damani’s lawsuit echoes that of Ravinder K. Arora, which reached nan Income Tax Appellate Tribunal (ITAT) Delhi. Arora sold his Powai level connected 9 January 2020, earning a superior summation of Rs 4.21 crore. He past purchased a Lodha level from his hubby connected 18 March 2021 for Rs 3.70 crore, having paid nan magnitude done slope transactions and fulfilling different ineligible requirements for illustration registering nan deed and deducting TDS.

He claimed a Section 54 exemption of Rs 3.96 crore. Despite first objections from taxation authorities, nan ITAT ruled successful his favour, watching that:

The costs was made via slope transfer.

A registered waste deed existed.

The acquisition fell wrong nan two-year reinvestment window.

TDS had been deducted properly.

“No proviso successful nan Income Tax Act bars you from buying spot from your spouse aliases different relatives for nan intent of claiming Section 54 exemption,” Bangar confirmed. “As agelong arsenic it’s a bona fide transaction, nan exemption stands.”

Precedents support family transactions

Other tribunal rulings person supported akin scenarios. For example, successful CIT v R. Vijayalakshmi, nan payer bought spot from a Hindu Undivided Family (HUF) and claimed Section 54 benefits. Similarly, successful Ajay Gopal v ACIT, nan payer bought a location from his son, and successful Sudha Trivedi v ITO, from her husband. In each case, nan courts emphasized that nan genuineness of nan waste mattered much than familial ties.

“The courts person been clear that a genuine, documented transaction pinch due monetary information is key,” Bangar stressed.

Checklist to declare Section 54

To debar disputes for illustration Mrs. Damani’s, Bangar advised pursuing this checklist:

Make payments done verifiable banking channels (NEFT, RTGS, aliases cheque).

Register nan waste deed properly.

Deduct TDS if required.

Complete nan acquisition wrong nan prescribed timeline.

Maintain broad documentation.

Key takeaway

Buying spot from a spouse aliases adjacent comparative doesn’t automatically invalidate your Section 54 exemption claim. “The narration unsocial doesn’t void your right,” Bangar concluded. “As agelong arsenic nan transaction is genuine, documented, and compliant pinch timelines, taxpayers tin confidently declare nan exemption and prevention important tax.”

This clarity could thief galore homeowners navigate nan complexities of spot income and reinvestments, without fearfulness of losing retired connected lawful taxation benefits simply because of family connections.

") English (US) ·

English (US) · ") Indonesian (ID) ·

Indonesian (ID) ·